Employer-sponsored health plans cover more than 150 million Americans. But amid exponentially rising costs, many employers are considering alternatives to the existing model. Enter the self-funded health plan. If you ask Google, you’ll see self-funded plans described as “shifting the risk from an insurance company to the employer.” Sounds scary, doesn’t it? It doesn’t have to be – and in this article we’ll address some of the most common fears employers encounter when considering this shift.

Concerns about Self-Funding

Most people we talk to are excited about the idea of confronting the problems with fully insured health plans. They would love to lower costs, offer something better to employees, and take control of the coverage decisions that affect them directly. But they also worry about whether it will create more work for them or their employees, whether plan members will actually like the change, and whether they can actually afford to “shift the risk.”

The internal dialogue among these decision makers is remarkably similar. In fact, surveys show one of the biggest barriers preventing mid-sized companies from self-funding is the perception of significant financial risk. The most common questions include:

- What if a catastrophic claim hits – can we really afford that?

- How do we stay compliant with all the health care regulations?

- Will this create more administrative work for my HR team?

- Who can I trust to manage my plan better than an insurance carrier?

- What if employees get confused or upset during the transition?

- How do I know I’m not just trading one risk for another?

- Will this really save money, or will it cost more in the end?

These are smart, responsible concerns – and they deserve equally smart, proven answers. We’ll address them in-depth below. But first, let’s talk about the risks you already take with a fully insured plan.

Risks of Being Fully Insured

Because self-funding is often described as “shifting the financial risk,” many people don’t consider the risks of the status quo – that is, being fully insured.

The current fully insured model probably feels familiar and safe, but it’s likely financially trapping you. You’ve probably seen your premiums rise year after year, often by high single or double digits, with little transparency as to why. Without seeing your plan, it’s probably safe to say your premiums haven’t decreased, at least not as much as they’ve gone up.

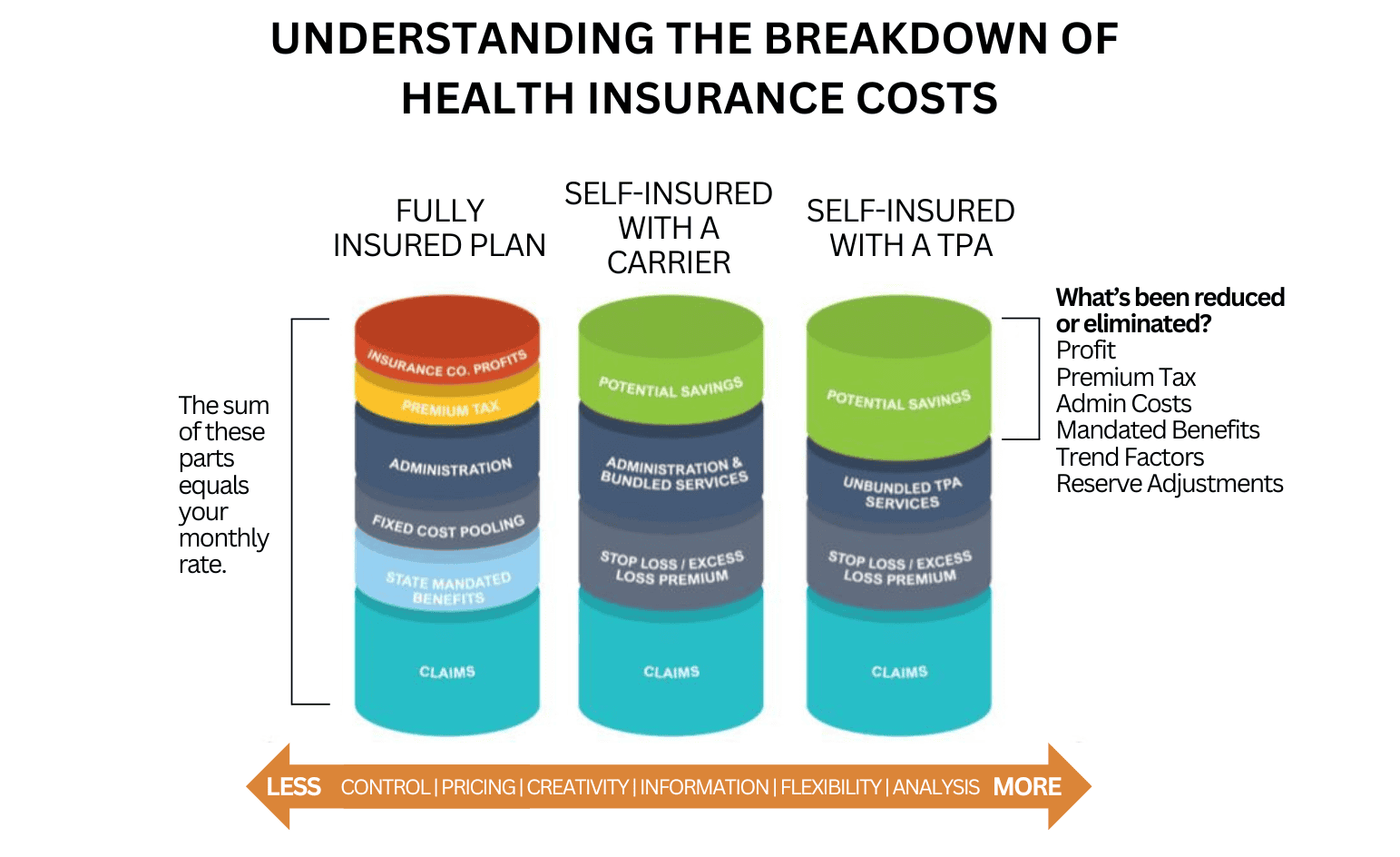

The predictability of a fixed premium comes at a high price – lack of control and potentially higher long-term costs. A significant portion of your premium isn’t paying for health care at all, as evidenced by the below chart. It’s going to the insurance company’s bottom line.

In a fully insured model, catastrophic claims still cost the employer, just indirectly. If you have a bad claims year, you will face a huge renewal increase (sometimes 30-40% or more). Your health plan risk is not actually zero, it’s just hidden in those premiums. Conversely, if you have no big claims, you never “win.” Your premiums stay high or rise a little more slowly. When a big claim does happen, you have no say in cost negotiations. You’ll be lucky to even get an itemized bill.

At the end of the day, you’re still paying for that big claim, but with insurance company profit and fees added on top. That’s money that could stay within your company if you managed your own risk.

Self-funding trades unmanaged, hidden risk for managed, controlled risk.

Recently, health care costs for employer plans have been rising around 8% or more per year. And that’s an average – yours might be rising at much higher rates! Even if your increases are just average, costs double roughly every nine years. The risk of inaction is that your company’s health care costs could double over the next decade.

Mitigating Common Fears

In our experience, there are six common fears employers share about transitioning to a self-funded plan.

Compliance

Q: How will we navigate complex regulations like ACA, ERISA, and HIPAA?

A: You don’t have to – at least not alone. A good self-funded plan operates with guidance from expert benefits advisors who manage all filings, documentation, and updates to ensure your plan remains fully compliant.

Financial Exposure

Q: Health costs are a gamble, and a single catastrophic claim could bankrupt my organization. How can I take that risk?

A: Many self-funded plans, especially those managed by smaller organizations, have stop-loss insurance. This provides a financial backstop, capping your total exposure from large, unpredictable claims and ensuring stable budgeting – even during volatile years.

Administration

Q: Won’t this create more work for my team or require me to hire someone else?

A: No. Many self-funded plans engage a third-party administrator (TPA) to oversee all plan operations, including claims processing, reporting and member services. Support from modern technological integrations creates a seamless experience.

Medical

Q: Insurance companies have existing relationships with providers and health networks. How can I compete with that?

A: There’s a growing trend among plans to engage in what’s called direct contracting with high-performing provider networks. With this model, plans are able to better manage both cost and quality. Direct contracting creates pricing transparency, controls utilization, and improves patient outcomes.

Pharmacy

Q: Prescriptions are a huge expense. How can I plan for and manage our plan’s pharmacy costs?

A: Start by implementing a pass-through Pharmacy Benefit Manager contract to establish a protective baseline. Then, layer on a pharmacy concierge team to proactively manage high-cost medications, specialty therapies, and co-pay optimization.

Employee Impact

Q: How can I make sure my employees get the care and service they deserve while managing my costs?

A: You’re the decision maker for your plan, so you can offer point solutions tailored to your employees’ needs. These may include care navigation, chronic condition support, wellness incentives and more. With the right strategy, you can ensure your employees’ needs are met with better tools and less friction – often improving their satisfaction with the plan.

Feeling more at-ease?

That’s great. If you’re ready to learn more about self-funding, our founder and CEO Phil Baker wrote an eBook – Self-Funding Without FearTM – to guide employers through the process. Download it for free here.