Employer-sponsored health insurance is a staple of many employee benefits packages. These plans covered more than 150 million Americans in 2024, according to research by the Kaiser Family Foundation. Behind salaries, it’s usually one of any organization’s largest employee-related expenses.

But not all plans are the same. Employer-sponsored plans typically fall into one of two categories: fully insured and self-funded.

- Fully insured health plans are completely managed by an insurance company. An employer offering a group plan simply purchases insurance directly from Blue Cross Blue Shield, Cigna, Aetna, United Healthcare or a similar company. Prices are set by the insurer. Premiums are paid to the insurer. Claims are paid by the insurer. All regulations and other administrative duties are managed by the insurer. And profits belong to the insurer.

- Self-funded health plans belong to the sponsoring organization, with support from various partners. Prices are set by the organization. Premiums are paid into an internal fund. Claims are paid from those funds. Regulations and other administrative duties may be structured differently, depending on the organization, but management often involves a mix of internal teams and external partners. And all profits belong to the sponsoring organization.

The Problem with Fully Insured Health Plans

This section is probably better titled the problems (plural). There are many. A few of the most prominent, and the ones we’ll address here, are:

- The cost – Employer-sponsored plans are costly, with the average plan priced around $9,000 for a single member and $25,000 for a family. Premiums rise consistently and significantly – more than 50% in the last decade alone – and increases often outpace wages.

- Health decisions in the hands of a third-party – With typical health insurance plans, the insurance companies usually oversee coverage decisions. They dictate everything from which providers and facilities are in-network to what medications and procedures may be covered. And there may be multiple third parties involved.

- Complex webs of red tape that make the plan tough for employees to navigate – Insurance companies aren’t known for their stellar customer service. Add to that the countless point solutions you probably have in a futile attempt to lower premiums, and the plan can be a nightmare to deal with.

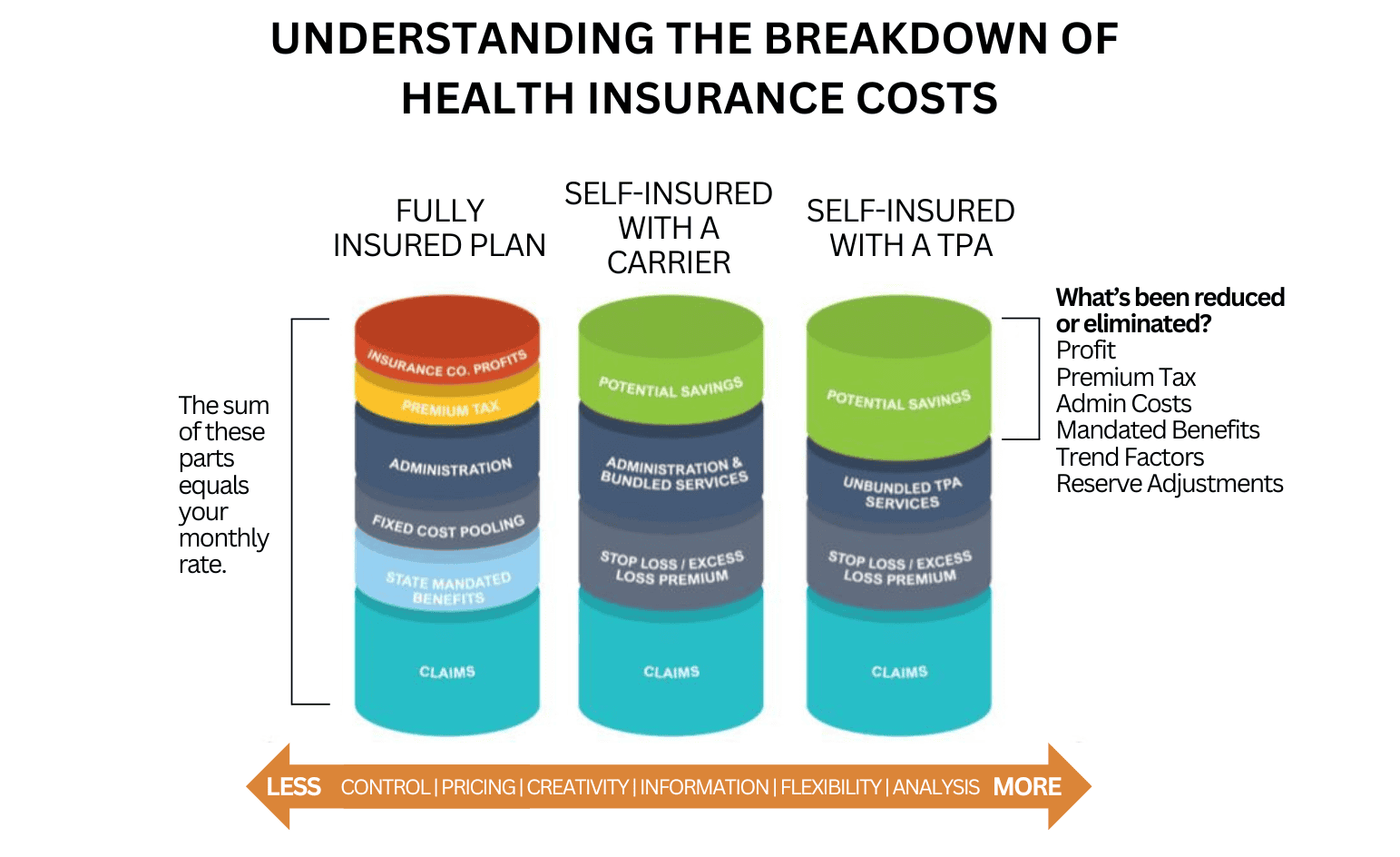

Cost Breakdown: Fully Insured vs. Self-Funded Health Plans

Not all health plans have the same costs. The prices may be similar, but where the money goes varies depending on the plan type.

Premiums on fully insured plans go toward:

- Claims

- State-mandated benefits – This varies by state, but it includes things like requiring coverage for certain procedures, prescriptions, and groups of people, among other mandates.

- Fixed cost pooling – Insurance companies set rates by “pooling” your organization with others to calculate a monthly cost, which remains the same through the insurance year, regardless of whether your actual claims are higher or lower.

- Administration

- Premium tax – This is a tax on the premium itself, and self-insured plans are typically exempt.

- Insurance company profits

Premiums on self-funded plans go toward:

- Claims

- Stop-loss (or excess loss) premiums – This “insurance for your insurance” protects your organization from catastrophic claims.

- Either administrative costs and bundled services or unbundled services through a third-party administrator, depending on the structure of the plan

Because self-funded plans are often exempt from regulations like state-mandated coverage and premium taxes, they have a built-in cost advantage. The gap widens considerably when things like insurance company profits or fixed cost pooling come into play – because self-funded plans reap the benefits of those related savings, rather than feeding another company’s bottom line.

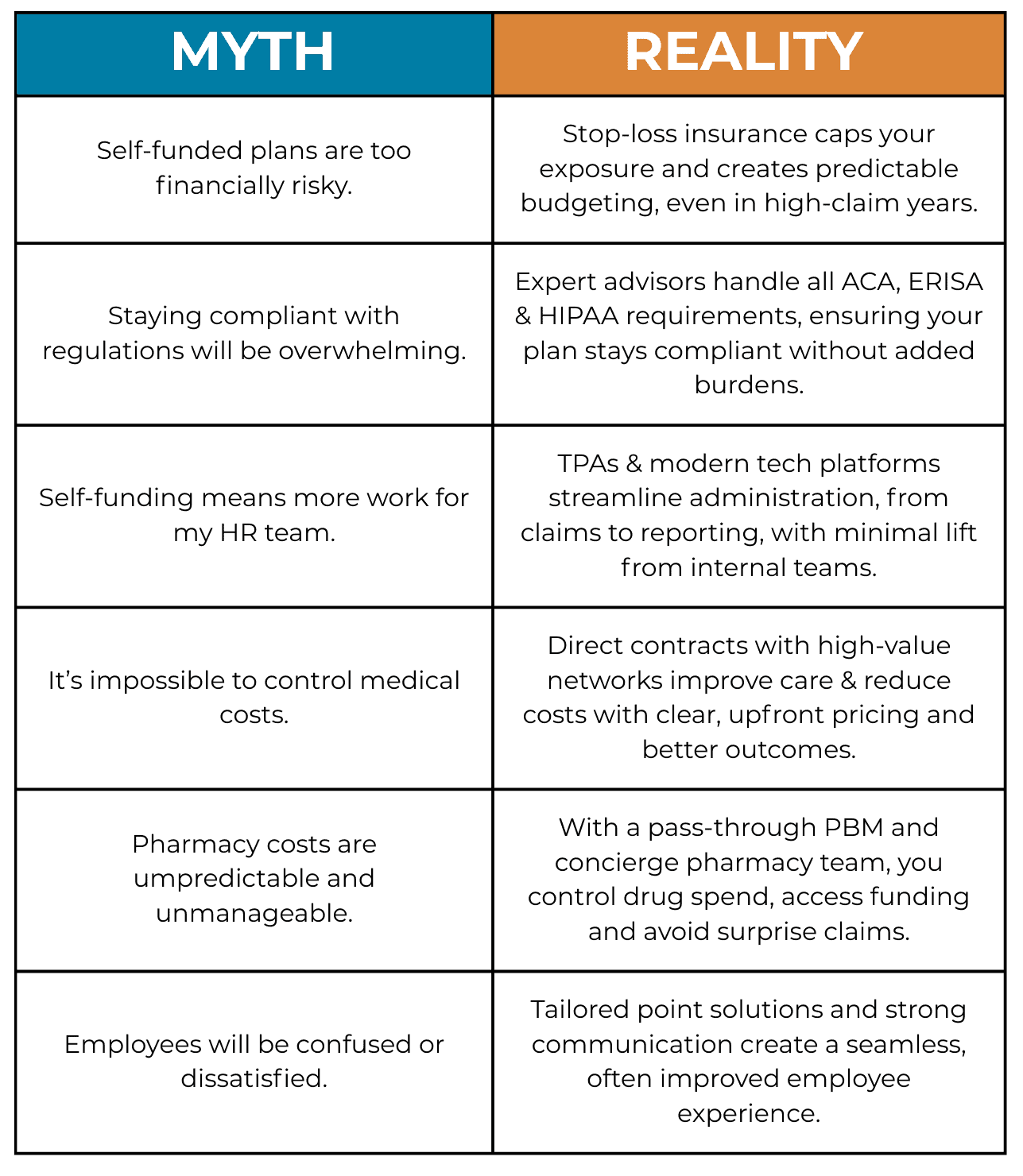

Myths vs. Realities of Self-Funded Health Plans

A well-designed self-funded plan can out-perform fully insured models on cost, control, and employee satisfaction. Some of the most common myths unravel quickly in the face of real data and strategies.

Is a Self-Funded Plan a Good Idea for My Company?

A well-designed self-funded plan can out-perform fully insured models on cost, control, and employee satisfaction. Some of the most common myths unravel quickly in the face of real data and strategies, and it’s often at least worth considering. But we’ll address the details in another article.

Ready to Learn More?

Phil Baker, founder of HaloScrips and Good Shepherd Health Institute, wrote an eBook – Self-Funding Without FearTM – to guide employers through the process. Download it for free here.